In the National Economics Challenge (NEC), capital-flow questions in the world-economy section test one idea: money chases the highest risk-adjusted return, so it moves across borders toward better expected yields, safer institutions and growth. Get the drivers right — interest-rate gaps, return on investment, risk and expectations — and you can reason through any foreign-investment scenario without inventing a figure.

What “capital flows” mean in the NEC world-economy section

The NEC, run by the Council for Economic Education (CEE, founded 1949), covers microeconomics, macroeconomics and the world/international economy and reaches roughly 10,000 students a year in the United States. Its world-economy questions reward a clean model over memorised numbers. A capital flow is the movement of financial capital across a border — a saver, firm or fund in one country acquiring an asset, a stake, or a loan claim in another.

The NEC typically asks you to separate two kinds of cross-border investment, because they behave very differently under pressure:

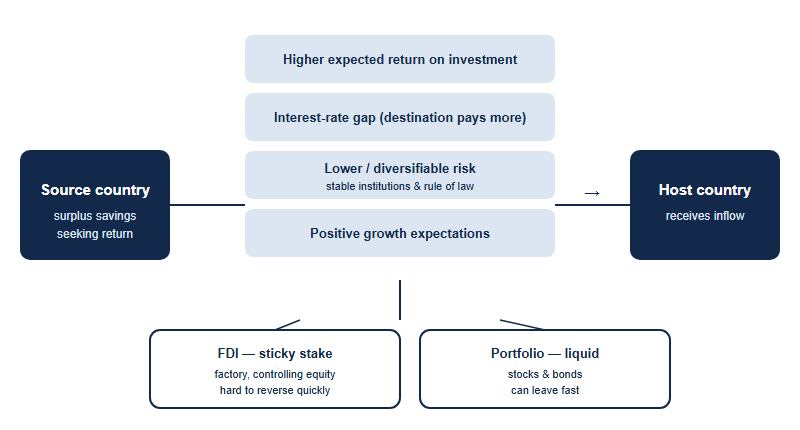

- Foreign direct investment (FDI) — a lasting, controlling stake: building a factory, acquiring a company, or owning a meaningful share of voting equity. FDI is “sticky” and hard to reverse quickly.

- Portfolio investment — buying foreign stocks or bonds for a financial return without control. It is liquid and can leave fast (“hot money”).

- Other flows — cross-border bank loans and deposits, plus changes in official reserves.

A common NEC trap is treating all inflows as identical. A $1bn greenfield factory and $1bn of bond purchases both count as capital inflows, but the factory creates local jobs and transfers technology, while the bond position can be sold and withdrawn in days. The exam rewards students who can say which type of capital a scenario describes and why that matters for jobs, stability and policy.

Why capital moves across borders

The exam wants drivers, not anecdotes. Capital leaves a country with surplus savings and limited domestic opportunities, and is pulled toward a destination offering a better deal. The four levers NEC questions lean on are:

- Expected return on investment — a fast-growing economy with under-served markets offers higher returns on a new plant or stake than a saturated mature market.

- Interest-rate differentials — if assets abroad pay a higher rate than at home, savers move funds to capture the spread. (A rate change therefore moves the currency too — the FX mechanics behind that are a separate topic.)

- Risk — political stability, rule of law, contract enforcement and predictable policy lower the risk premium investors demand. Investors also flow in to diversify, spreading exposure across uncorrelated economies.

- Expectations — beliefs about future growth, currency direction and policy can move money before any fundamentals change. This is why “hot money” can reverse on sentiment alone.

A high-scoring NEC answer names the relevant lever, states the direction of the flow, and traces one knock-on effect — for example, “higher domestic interest rates attract portfolio inflows, which is more reversible than FDI and so adds less to long-run productive capacity.” That chain of reasoning is exactly what graders reward.

Effects on host and source economies

Capital flows are not automatically good or bad; the NEC tests whether you can weigh both sides. For the host (recipient) economy, inflows can fund investment beyond what domestic savings allow, while FDI specifically brings managerial know-how, supply-chain links and technology transfer that pure financial flows do not. The risks are real too: a sudden stop or reversal of liquid “hot money” can drain reserves and force painful adjustment, and heavy reliance on foreign capital can leave a country exposed to shifts in global sentiment it cannot control.

For the source economy, sending capital abroad earns returns that flow back later as income, and gives investors diversification — but it can also mean less capital deployed at home. The table below is the kind of two-sided ledger NEC questions expect you to reproduce under time pressure.

| Dimension | Host (receiving capital) | Source (sending capital) |

|---|---|---|

| Main benefit | Funds investment beyond domestic savings; FDI adds jobs & technology | Earns foreign returns; diversifies risk across economies |

| Productive spillovers | Know-how, supply chains, competition raises standards | Firms access larger global markets and cheaper inputs |

| Key risk | Sudden reversal of hot money; over-reliance on foreign capital | Less capital invested at home; exposure to foreign political risk |

| Stability driver | FDI far more stable than portfolio flows | Returns depend on host's policy and currency path |

Notice the recurring theme: FDI is more stable than portfolio investment. That single contrast resolves a large share of capital-flow questions, because it predicts how an economy behaves when global conditions tighten.

The link to the financial account

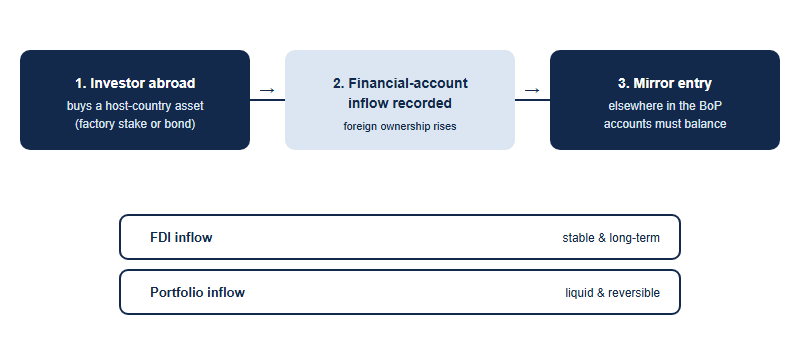

Every cross-border flow is recorded somewhere in a country's external accounts. Capital and foreign-investment transactions land in the financial account — the part of the balance of payments that tracks changes in cross-border ownership of assets. The accounting identity that ties the financial account to the current account, and what a “surplus” or “deficit” in each really means, is a distinct topic; here, focus on the economic logic that drives the flows in the first place.

The bridge worth memorising is this: a country that consistently receives more capital than it sends is, by definition, recording net inflows on its financial account — and that financial-account position has a mirror image elsewhere in the accounts. NEC questions often hand you a flow and ask which account moves; tie “foreign investment in” to “financial-account inflow” and you will rarely be wrong. For the accounting frame itself, see our companion explainer on how the NEC tests the balance of payments.

How to practise this for the NEC

A worked example first. To see the template in action, take a typical NEC-style prompt: “Country A raises its central-bank interest rate while a multinational simultaneously announces a new manufacturing plant in Country A. Explain the likely capital-flow effects.” A weak answer says “more money comes in.” A high-scoring answer separates the two flows and reasons about each.

First, the rate rise. Higher domestic rates widen the interest-rate differential, so yield-seeking portfolio capital flows in to capture the spread. This inflow is liquid: if the rate gap narrows later, the same money can leave just as quickly, so it adds little durable productive capacity. Second, the new plant is FDI — a sticky, controlling investment driven by expected return and the host's market access. It builds capacity, hires locally and may transfer technology, and it will not reverse on a sentiment swing. Both are financial-account inflows, but only one strengthens the economy's long-run base.

The strongest answers then add the two-sided caveat: the portfolio inflow leaves Country A more exposed to a sudden reversal, while the FDI improves resilience. That is the full arc the NEC rewards — classify, name the driver, weigh both sides, and place each flow in the financial account. Memorising a country's actual inflow figure would not help here; the reasoning does all the work, which is precisely why the world-economy section is built this way.

Capital flows reward structured reasoning, so practise the moves rather than facts. As the official China National Round, CNEC — run by Hanlin (SKT) as the officially authorized China test center since 2016, across 20+ provinces and 300+ schools — is the route Chinese students take toward the NEC global rounds, and the skills below transfer directly across the qualifying test, Critical Thinking and quiz rounds.

- Classify first. On any scenario, label the flow: FDI, portfolio, or bank lending. Half the marks follow from naming the type correctly.

- Name the driver. Tie the flow to one of the four levers — return, rate gap, risk, or expectations — and state the direction.

- Trace two-sided effects. Always give a benefit and a risk for both host and source; graders reward balance, not cheerleading.

- Map to the account. Finish by placing the flow in the financial account, so your answer connects micro logic to the macro picture.

Work past world-economy items this way and you build a repeatable template that holds whatever numbers a question throws at you. For division formats and the seven rounds, start at the CNEC overview, and confirm current dates and rules on the official CNEC channels.

Frequently asked questions

What is the difference between FDI and portfolio investment in the NEC?

FDI is a lasting controlling stake (a factory or company); portfolio investment is liquid stocks and bonds bought for return without control.

Why does capital move across borders?

It chases higher risk-adjusted returns — driven by expected return, interest-rate gaps, lower or diversifiable risk, and growth expectations.

Are capital inflows good for the host economy?

They can fund investment and bring technology, but liquid “hot money” can reverse suddenly; FDI is far more stable than portfolio flows.

Which account records foreign investment?

The financial account, part of the balance of payments, tracks changes in cross-border ownership of assets — so foreign investment in equals a financial-account inflow.

Published by the NEC / CNEC editorial desk, operated by Hanlin Education as the officially authorized China National Economics Challenge (CNEC) test center. The NEC is run by the Council for Economic Education, which sets the official rules — always confirm current dates, divisions, fees and awards on the official CNEC channels. Any error is corrected within 7 working days.