The National Economics Challenge (NEC) tests money and banking as a set of mechanics: commercial banks create money when they lend out part of every deposit, the money multiplier turns the central bank's reserves into a larger stock of deposits, and the financial system channels savings to borrowers who invest. The marks reward knowing how a deposit multiplies, what counts as money, and why a bank is more than a vault — not memorizing the central bank's policy tools.

How commercial banks create money

The single most-tested idea in this corner of the syllabus is that money is created by ordinary banks, not just printed by the central bank. In a fractional-reserve system a bank holds only a fraction of each deposit as reserves and lends the rest. That loan becomes someone else's deposit at another bank, which keeps its own fraction and lends again, and the cycle repeats. No new paper is printed; the money supply still expands, because deposits are money and each loan manufactures a fresh deposit. NEC items reward a student who can name this process precisely and trace it one or two rounds through the banking system.

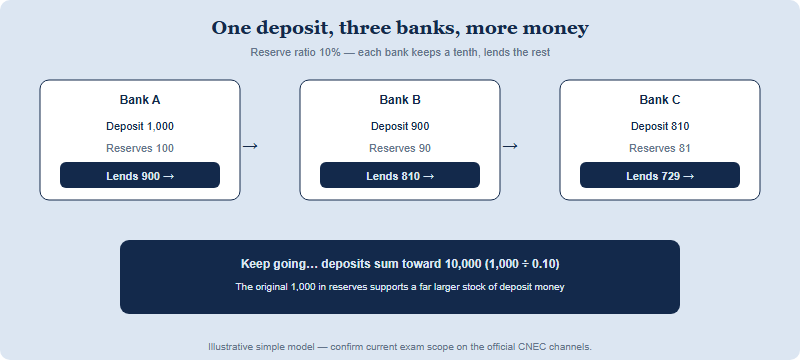

The cleanest way to show it — and the format examiners use — is a bank balance sheet (a T-account), where assets equal liabilities. A new deposit lands as a liability the bank owes the customer; the bank splits it into required reserves (an asset it must hold) and a loan (an asset that earns interest). Suppose the required reserve ratio is 10% and a customer deposits 1,000 currency units. The bank keeps 100 in reserves and lends 900. That 900 is spent and redeposited, the next bank keeps 90 and lends 810, and the chain continues with smaller amounts each round. Two distinctions seed most of the distractors:

- A single bank can only lend out its excess reserves (the deposit minus required reserves), but the whole banking system can expand deposits by a multiple of the original reserve injection.

- Cash a customer deposits is not new money — it was already money. The new money is the deposits the loans create on top of it.

The Council for Economic Education (CEE), founded in 1949, sets the academic standard the NEC is built on, and treats money and banking as core macroeconomics alongside the micro and world-economy material; you can see where these threads sit on the CNEC home page.

The money multiplier: deriving the ceiling

Once the chain is clear, NEC items ask you to derive the total, not add fractions forever. The money multiplier (in its simple form) is the reciprocal of the required reserve ratio: with a ratio of 0.10 the multiplier is 1 ÷ 0.10 = 10, so an injection of 1,000 in fresh reserves can support up to 10,000 in deposits. A discriminating question gives you the ratio and asks for the multiplier, or hands you the multiplier and a reserve injection and asks for the maximum change in the money supply. Note the framing: this multiplier governs money creation by the banking system, which is a different question from the spending multiplier in fiscal items, where the leakage is the marginal propensity to save.

The marks that separate strong competitors sit in the word maximum. The simple formula assumes banks lend every spare cent and the public redeposits everything. In reality two leakages shrink the result: banks may hold excess reserves rather than lend them all, and the public may hold some money as cash rather than redeposit it. Both reduce the effective multiplier below the textbook ceiling. NEC reasoning rounds reward a student who computes the simple multiplier and then names why the realized expansion is smaller — without quoting a specific real-world figure, which should always be checked against current official material rather than assumed.

| Required reserve ratio | Simple money multiplier (1 ÷ ratio) | Max deposits from 1,000 in reserves |

|---|---|---|

| 20% (0.20) | 5 | 5,000 |

| 10% (0.10) | 10 | 10,000 |

| 5% (0.05) | 20 | 20,000 |

The pattern examiners want you to read off the table is the inverse relationship: a lower reserve ratio means a larger multiplier and more potential deposit creation. The numbers above are arithmetic illustrations of the formula, not policy figures to quote.

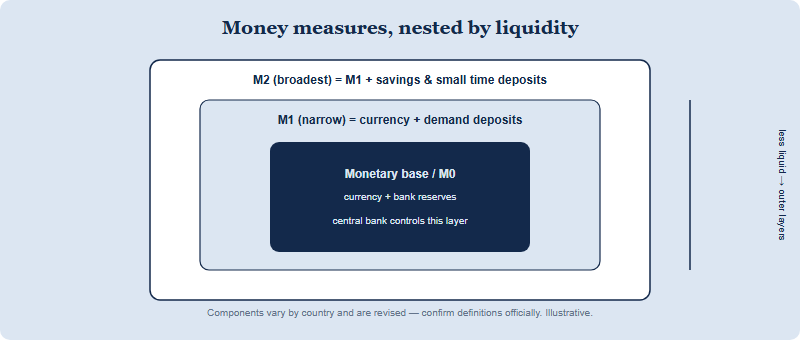

Measuring the money supply: M0, M1 and M2

If banks create money, NEC then asks: what counts as money, and how is it measured? The standard answer is a set of nested monetary aggregates ordered by liquidity. The monetary base (often labelled M0) is the most basic layer: physical currency plus bank reserves — the raw material the central bank controls directly. M1 is the narrow, most-liquid measure: currency in circulation plus checkable (demand) deposits — money you can spend immediately. M2 is broader: M1 plus less-liquid stores such as savings deposits and small time deposits — money that is close to spendable but not instantly so. The exact components of each aggregate vary by country and are periodically revised, so the precise definitions should be confirmed on official sources; the ordering by liquidity is the durable, examinable idea.

The conceptual hook examiners reward is the difference between the base and the broad measures. The central bank controls the monetary base directly; the banking system, through the lending process above, turns that base into the much larger M1 and M2 the public actually uses. That is precisely why the money multiplier matters — it is the bridge from the base the central bank sets to the broad money the economy spends. A frequent NEC distractor treats a credit card's limit as money: it is not, because it is a way to borrow, not a stock of money you hold.

- Monetary base / M0 — currency plus bank reserves; the layer the central bank controls.

- M1 (narrow) — currency in circulation plus demand deposits; immediately spendable.

- M2 (broad) — M1 plus savings and small time deposits; near-money.

The financial system: why a bank is more than a vault

The fourth strand NEC tests is the role of the financial system — the network of banks and markets that links savers and borrowers. Its core economic job is intermediation: gathering the savings of many households and channeling them to firms and individuals who want to invest. This is the bridge to the rest of macroeconomics, because it is how saving becomes investment in new capital. Examiners reward a student who can explain the functions a bank performs beyond holding cash, and who connects financial intermediation to growth.

Three functions recur in well-set items. Banks provide maturity transformation — they take deposits that can be withdrawn at short notice and make longer-term loans, reconciling savers who want liquidity with borrowers who need time. They perform risk pooling and screening — spreading funds across many loans and assessing who is creditworthy, which an individual saver could not do alone. And they lower transaction and information costs — it is far cheaper to deposit at a bank than to find and vet a borrower yourself. Markets for bonds and equities sit alongside banks as a second channel from savers to firms. A strong NEC answer frames the financial system as the machinery that turns idle savings into productive investment, and notes that its failure — a credit freeze or bank run — can choke that flow. For how these macro threads connect across the syllabus, see the CNEC editorial section.

| Function | What the bank does | Why it matters economically |

|---|---|---|

| Intermediation | Pools savings, lends to investors | Turns saving into investment |

| Maturity transformation | Short-term deposits fund longer loans | Liquidity for savers, time for borrowers |

| Risk pooling & screening | Spreads and assesses credit risk | Capital reaches creditworthy uses |

How money-and-banking items appear across the NEC rounds

This material is not confined to one part of the competition; it surfaces across the seven rounds — Qualifying Test, Super Econ, Quiz Bowl, Critical Thinking, Econ Lab, Econ Immersion and U20 Youth Voice — and the round changes the kind of question it sets. In the timed multiple-choice and buzzer rounds, expect crisp calculation and definition items: compute the money multiplier from a reserve ratio, identify which aggregate a demand deposit belongs to, state how a deposit expands through the banking system. In the analytical and applied rounds, expect a scenario — a bank balance sheet to read, or a prompt to explain how the financial system channels savings to investment, or why holding excess reserves shrinks the realized multiplier.

For a China team preparing through CNEC — the official China National Round, operated by Hanlin (SKT) since 2016 across 20+ provinces and 300+ schools, and the only official path from China into the NEC global rounds — the practical lesson from running the round is concrete. The recurring slip our CNEC teams make is not the arithmetic; it is confusing the single bank with the whole system — computing a maximum expansion for one bank, or treating the central bank as the direct creator of all money rather than as the supplier of the base that banks multiply. We coach teams to anchor every money item to one question first — one bank, or the system? — and to compute the simple multiplier and then name the leakages that pull the real figure below it. Round formats and weightings can change between seasons, so confirm the current structure on the official CNEC channels before building a prep plan around it.

- Calculation register — multiplier from the reserve ratio; maximum deposit expansion from a reserve injection. Train these to reflex for the buzzer.

- Classification register — place an asset in M0, M1 or M2 by its liquidity; reject "near-money" traps such as credit limits.

- Explanation register — in open rounds, describe intermediation and the leakages (excess reserves, cash holdings) that bound real money creation.

FAQ

How do commercial banks create money?

By lending out part of each deposit under fractional reserves; each loan becomes a new deposit elsewhere, so the banking system expands the money supply.

How do you calculate the simple money multiplier?

It is the reciprocal of the required reserve ratio, so a 10% ratio gives a multiplier of 1 ÷ 0.10 = 10 deposits per unit of reserves.

What is the difference between M1 and M2?

M1 is the narrow, most-liquid money — currency plus demand deposits. M2 adds less-liquid savings and small time deposits.

What is the main role of the financial system?

Intermediation: it channels savers' funds to borrowers who invest, transforming maturity and pooling risk to turn saving into investment.

Published by the NEC / CNEC editorial desk, operated by Hanlin Education as the officially authorized China National Economics Challenge (CNEC) test center. The NEC is run by the Council for Economic Education, which sets the official rules — always confirm current dates, divisions, fees and awards on the official CNEC channels. Any factual error will be corrected within 7 working days.