On the National Economics Challenge (NEC), cost and production theory is tested less as a set of formulas to recall and more as a logic to apply: given a firm's output, you should be able to trace its fixed, variable and marginal costs, distinguish the short run from the long run, and explain why average cost first falls and then rises through economies and diseconomies of scale. This guide walks through the cost side of microeconomics the way the NEC frames it.

Why costs sit at the heart of NEC microeconomics

The NEC is run by the Council for Economic Education (CEE), founded in 1949, which sets the academic standard the contest is built on. Its three subject pillars are microeconomics, macroeconomics and world / international economy, and the theory of the firm's costs is load-bearing inside the micro pillar. The reason is mechanical: a firm maximises profit where marginal revenue equals marginal cost, so you cannot find the profit-maximising output, judge a shutdown decision, or explain a supply curve without first understanding how costs behave as output changes.

For students entering through CNEC — the official China National Round operated by Hanlin (SKT) since 2016, and the only official path from China to the NEC global rounds — costs are also where many first-time competitors lose marks they should keep. They can write the definition of marginal cost but stumble when a question asks why the marginal cost curve cuts the average cost curve at its lowest point, or whether a loss-making firm should keep producing. The relationships, not the definitions, are the test. You can review how the wider contest is organised on the CNEC homepage.

Start with the vocabulary the NEC assumes you already own. Every cost measure is built from two raw ingredients and then sliced into totals, averages and a margin:

- Fixed cost (FC): does not change with output — rent on a factory, an insurance premium, a loan repayment. It exists even at zero output and only appears in the short run.

- Variable cost (VC): rises as output rises — raw materials, hourly wages, electricity for the production line.

- Total cost (TC = FC + VC): the whole bill at a given output.

- Average total cost (ATC = TC ÷ Q): cost per unit — the number you compare against price to see profit per unit.

- Marginal cost (MC): the extra cost of producing one more unit. This is the decision-maker's number, because firms optimise at the margin.

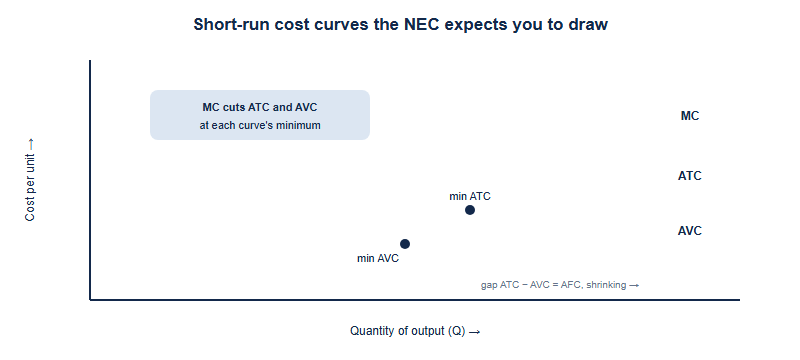

The marginal-average relationship: the single most tested idea

If there is one cost result the NEC returns to, it is the geometry above: the marginal cost curve intersects the average total cost and average variable cost curves at their lowest points. This is not a coincidence to memorise — it is a logical certainty, and graders reward students who can say why.

The intuition is the same one used for a test average. If your next exam score (the marginal value) is below your running average, it drags the average down; if it is above, it pulls the average up. So whenever MC is below ATC, ATC falls; whenever MC is above ATC, ATC rises. The only point where the average is neither rising nor falling — its minimum — is exactly where the marginal equals the average. The same logic forces MC through the minimum of AVC.

Two more relationships round out the short run, and both flow from the law of diminishing marginal returns — the idea that, with at least one fixed factor, adding more of a variable factor eventually raises output by smaller and smaller increments. Because of this, marginal cost is U-shaped: it falls while early extra workers specialise and add a lot, then rises once the fixed plant gets crowded. And because average fixed cost (AFC = FC ÷ Q) keeps falling as the fixed bill is spread over more units, the gap between ATC and AVC narrows as output grows but never closes.

A reliable NEC exam habit: when a cost question appears, anchor on marginal cost first. Find where MC sits relative to the averages, and the shape and direction of every other curve follows.

Short run vs long run: the definition that trips students up

In economics the short run and long run are not calendar periods — a fact NEC scenario questions exploit. The distinction is about which inputs can be varied.

- Short run: at least one factor of production is fixed (typically capital — the plant, the machines). The firm can only change output by adjusting variable inputs such as labour and materials. This is the period where fixed costs and diminishing marginal returns apply.

- Long run: all factors are variable. The firm can change the size of its plant, enter or exit, and adopt different technology. There are no fixed costs in the long run — everything can be altered.

A classic NEC trap: a prompt mentions "over the next six months" and a weaker student labels it short run because six months feels short. But if the firm can build a new factory within that window, it is operating in the long run for that decision. What defines the long run is the ability to vary every input, not the number of weeks on the calendar.

| Feature | Short run | Long run |

|---|---|---|

| Inputs | At least one fixed (usually capital) | All inputs variable |

| Fixed costs | Exist (rent, insurance, loans) | None — all costs are variable |

| Driving law | Diminishing marginal returns | Economies / diseconomies of scale |

| Cost curve | U-shaped SRAC for a fixed plant size | LRAC: envelope of many SRAC curves |

| Firm can… | Change output via variable inputs | Change plant size, technology, enter / exit |

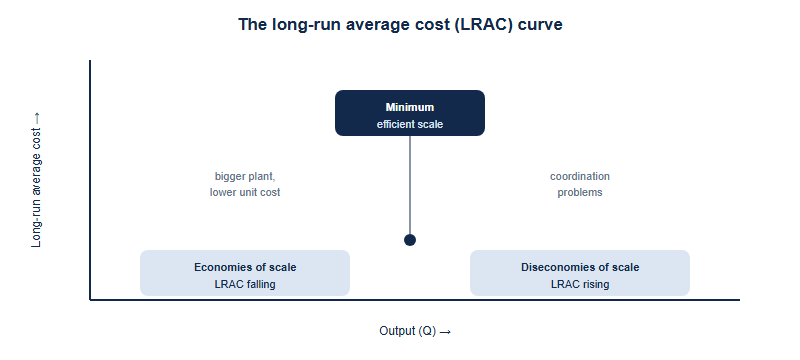

The link between the two periods is worth stating cleanly, because it sets up the next section. The long-run average cost (LRAC) curve is the envelope of all the short-run average cost curves the firm could choose — one short-run curve for each possible plant size. The firm, planning ahead, picks the plant whose short-run curve is lowest for the output it wants.

Economies of scale: why the long-run curve is U-shaped too

The shape of the LRAC curve is driven by returns to scale, and the NEC expects you to explain both halves of the U with concrete sources, not just labels.

Economies of scale (the downward-sloping part) mean long-run average cost falls as the firm gets bigger. Standard sources the contest looks for include:

- Technical: larger, more efficient machinery and the ability to specialise the division of labour.

- Purchasing: bulk-buying inputs at a discount — often called marketing or buying economies.

- Financial: large firms borrow more cheaply because lenders see them as lower risk.

- Managerial: employing specialists (a dedicated finance or logistics team) whose cost is spread over a large output.

- Risk-bearing: diversifying across products or markets so one setback does not sink the firm.

Diseconomies of scale (the upward-sloping part) mean average cost rises once a firm grows too large — usually from coordination and communication problems, slower decision-making, and weaker worker motivation in a sprawling organisation. Between the two lies the firm's minimum efficient scale (MES): the smallest output at which long-run average cost is minimised. A strong answer connects MES back to market structure — where MES is large relative to total demand, only a few firms fit, which is one structural reason some industries concentrate.

Watch the precise contrast the NEC likes to test: the short-run U comes from diminishing marginal returns to a variable factor against a fixed one; the long-run U comes from economies and diseconomies of scale when every factor varies. Same shape, completely different cause — conflating the two is one of the most common ways to lose an otherwise solid answer.

Putting costs to work: the shutdown and supply decisions

Cost theory earns its keep when the NEC asks a firm to make a decision. The headline application is the short-run shutdown rule, which trips up students who reason from profit instead of from the margin between price and average variable cost.

A firm that is losing money should keep producing in the short run as long as price covers average variable cost (P ≥ AVC). Why? Fixed costs must be paid whether or not it operates, so the only question is whether revenue covers the variable cost of staying open and makes some contribution toward the fixed bill. If price falls below AVC, every unit produced loses more than the fixed cost alone, so the firm shuts down. This is why the firm's short-run supply curve is its marginal cost curve above the minimum of AVC — a result the NEC frequently asks you to state and justify.

In the long run the bar rises: with no fixed costs, a firm only stays in the industry if price covers average total cost (P ≥ ATC). If it cannot, it exits. This is the cost-side engine behind long-run equilibrium — entry and exit push price toward minimum long-run average cost. Notice the discipline this demands: the NEC rewards you for reasoning from the right cost benchmark (AVC in the short run, ATC in the long run), not for jumping to "it's making a loss, so it should close."

A first-party note from the CNEC desk: where students lose marks

As the officially authorized China test center for the NEC, our coaching desk sees the same cost-theory slips every cycle. First, students recite that MC cuts ATC at its minimum but cannot explain the marginal-average logic that makes it inevitable — so they cannot adapt it when a question reshapes the curves. Second, they read "short run" as a length of time rather than as the period with a fixed factor, and mislabel decisions that are really long-run. Third, they confuse the cause of the two U-shapes, attributing the long-run curve to diminishing returns when it is driven by economies of scale.

A practical study sequence we use with CNEC teams: master the marginal-average relationship until you can derive it from the test-average analogy, then drill the short-run-versus-long-run distinction on scenario wording, and only then layer on economies of scale and the shutdown rule. The CEE sets the underlying academic standard the NEC is built on; the live contest structure — eligibility, divisions, rounds, dates, fees and awards — is published by the organiser, so confirm those on the official CNEC channels rather than inferring them. This article covers the microeconomics of costs and production only; market structures and factor markets are separate topics.

Frequently asked questions

Why does marginal cost cut average cost at its lowest point?

Because when the marginal value is below the average it drags the average down, and above it pulls the average up; equality occurs only at the average's minimum.

What is the difference between the short run and long run?

In the short run at least one factor is fixed; in the long run all factors are variable, so there are no fixed costs. It is about inputs, not calendar time.

What causes economies of scale?

Technical, purchasing, financial, managerial and risk-bearing advantages that lower long-run average cost as a firm grows, until diseconomies of scale set in.

Are costs and production part of NEC microeconomics?

Yes. The theory of the firm's costs is a core micro topic; NEC's subjects are microeconomics, macroeconomics and world economy. Confirm current scope on the official CNEC channels.

Published by the NEC / CNEC editorial desk, operated by Hanlin Education as the officially authorized China National Economics Challenge (CNEC) test center. The NEC is run by the Council for Economic Education, which sets the official rules — always confirm current dates, divisions, fees and awards on the official CNEC channels. Any errors will be corrected within 7 working days.