In the National Economics Challenge (NEC), exchange-rate-regime questions in the world-economy section test one judgement: a country choosing how to run its currency — fixed, floating or managed — cannot have everything it wants. Pick a regime and you accept a set of trade-offs. The exam rewards students who can name the regime, list what it buys and what it costs, and explain the “impossible trinity” behind the choice — without inventing a single figure.

Regime choice is a trade-off, not a setting

The NEC, run by the Council for Economic Education (CEE, founded 1949), covers microeconomics, macroeconomics and the world/international economy, and reaches roughly 10,000 students a year in the United States. Its exchange-rate questions reward reasoning rather than memorised data. An exchange-rate regime is simply the rule a government and central bank follow for setting the value of their currency against others. The key insight the test leans on is that this is a policy decision with costs, not a neutral technical choice: every regime hands the country some benefits and takes others away.

This is a different question from how the currency market itself clears, and from how cross-border flows are recorded. Those are separate strands — the day-to-day mechanics of appreciation and depreciation, and the accounting of the balance of payments, each sit in their own topic. Here the focus is narrow and high-value: given a scenario, which regime is in play, and what must the country give up to maintain it? Sorting that out is exactly the skill an analytical NEC round measures.

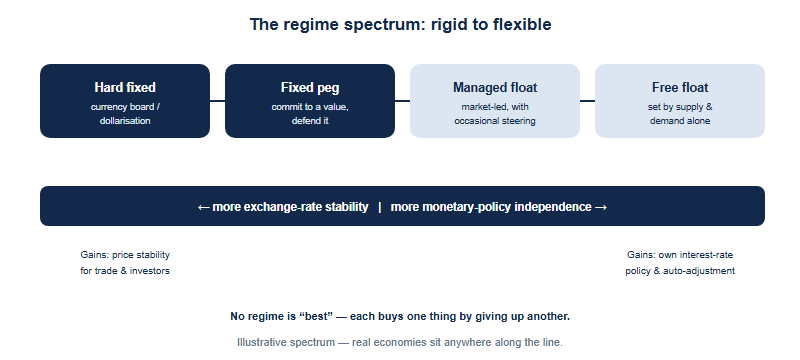

Fixed regimes: stability bought with lost autonomy

In a fixed (pegged) regime, the central bank commits to holding the currency at a set value against an anchor — another currency, or historically a commodity such as gold. To keep the peg, it stands ready to buy or sell its own currency using foreign-exchange reserves whenever market pressure pushes the rate away from target. A “hard” version, such as a currency board or full dollarisation, takes this to the extreme by locking the currency almost completely to the anchor.

The NEC expects you to state both sides of this bargain. The benefits are real: a fixed rate removes day-to-day currency uncertainty, which lowers risk for exporters, importers and foreign investors; it can anchor inflation by importing the credibility of a low-inflation anchor country; and it makes price comparisons across borders simple. The costs are equally real. The central bank largely surrenders an independent monetary policy — it must set interest rates to defend the peg rather than to cool or stimulate its own economy. It needs ample foreign-exchange reserves to defend the rate, and a determined speculative attack can drain those reserves and force a costly devaluation. And because the nominal rate cannot adjust, the burden of correcting an imbalance falls on domestic wages, prices and output instead.

Floating regimes: autonomy bought with volatility

In a floating regime, the exchange rate is determined by the market — the supply of and demand for the currency — with the central bank standing back. A pure free float involves no routine intervention; a managed float (sometimes called a “dirty” float) is mostly market-led but the central bank intervenes at times to smooth sharp swings or lean against a trend. Most large economies operate somewhere in the managed-to-free range — one reason the world-economy strand on the CNEC programme treats regimes as a spectrum rather than two boxes.

The trade-off flips. The headline benefit is monetary-policy independence: freed from defending a peg, the central bank can set interest rates for domestic goals such as managing inflation or supporting employment. A floating rate also absorbs external shocks automatically — if a country's exports fall, its currency tends to depreciate, which over time helps restore competitiveness without a wrenching internal adjustment — and it does not require a large war-chest of reserves to defend a line. The cost is exchange-rate volatility: the rate can move sharply, adding uncertainty for trade and investment, and a rapid depreciation can raise the price of imports and feed inflation. The exam reward is recognising that the float does not eliminate adjustment; it just changes where the adjustment shows up — in the currency rather than in domestic prices and jobs.

| Dimension | Fixed / pegged | Floating (free or managed) |

|---|---|---|

| Who sets the rate | Central bank commits & defends it | The market (supply & demand) |

| Monetary-policy freedom | Largely surrendered to defend the peg | Retained — set rates for domestic goals |

| Exchange-rate stability | High — predictable for trade | Lower — can swing with sentiment |

| Reserves needed | Large, to defend the rate | Small — no routine defence |

| How shocks are absorbed | By domestic wages, prices, output | By the currency adjusting |

| Main risk | Speculative attack → forced devaluation | Volatility → import-price & inflation swings |

The rows above are stable, conceptual contrasts to reason from, not figures to quote. A useful test-day rule: when a scenario hands a country a shock, ask where does the adjustment go? Under a peg it lands on the domestic economy; under a float it lands on the currency. Naming that channel is often the whole answer.

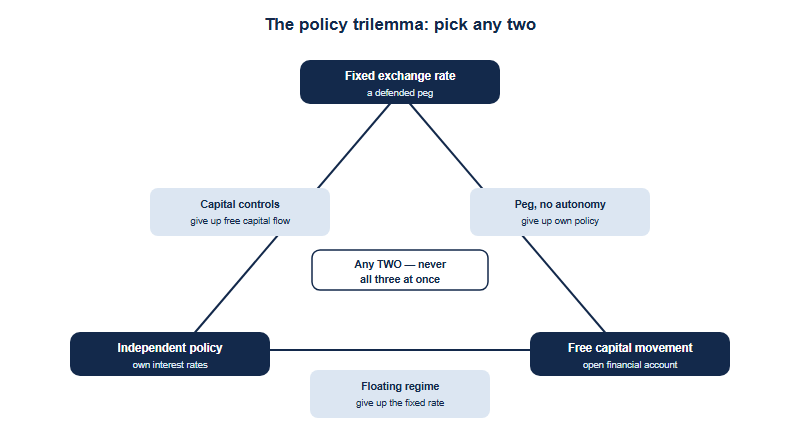

The policy trilemma: why you can't have all three

The deepest idea the NEC tests in this strand is the policy trilemma, also called the impossible trinity or the Mundell–Fleming trilemma. It states that a country cannot simultaneously have all three of: (1) a fixed exchange rate, (2) free movement of capital across its borders, and (3) an independent monetary policy. It can choose any two — never all three. This single framework explains why the regime choices above carry the costs they do, and it is the kind of structural reasoning that separates a top NEC answer from a list of pros and cons.

The logic is tight. Suppose capital can move freely and you also want to fix the rate. If you then cut interest rates to stimulate your economy (an independent policy move), money flows out chasing higher returns abroad; that selling pressure pushes your currency down, and to hold the peg you must buy your own currency until your reserves run low — so the independent move is unsustainable. You must give up one corner: float the currency (keep capital mobility + policy independence), impose capital controls (keep the peg + policy independence), or abandon independent policy and let interest rates serve the peg (keep the peg + capital mobility). The NEC rewards students who can take a described country, identify which two corners it has chosen, and explain which third it therefore had to surrender.

For where this world-economy material sits in the wider NEC syllabus, the three subject areas are laid out on the CNEC home page. The trilemma is worth over-learning because it ties micro-level intervention (buying and selling currency) to a macro-level constraint — exactly the cross-topic synthesis the analytical rounds prize.

A four-step routine for any regime question

NEC regime questions rarely ask for a textbook definition. They describe a country's situation — a peg under pressure, a policy choice, a shock — and ask you to reason about the trade-off. A repeatable routine turns any of them into a confident answer, whether the round is multiple-choice, a buzzer or a written response.

- Step 1 — Name the regime. Is the country fixed, floating or managed? Look for the tell: defending a value with reserves signals a peg; letting the market set it signals a float.

- Step 2 — State what it buys. A peg buys stability and an inflation anchor; a float buys monetary-policy independence and automatic shock absorption.

- Step 3 — State what it costs. A peg costs policy autonomy and reserves (and risks a forced devaluation); a float costs exchange-rate volatility and possible import-price inflation.

- Step 4 — Add the trilemma. Where the format allows, identify which two of {fixed rate, capital mobility, policy independence} the country has chosen and name the third it had to give up.

Worked example: “A country pegs its currency and allows capital to move freely. It then cuts interest rates to fight a recession. Why might the peg break?” Step 1, the regime is a fixed peg with open capital markets. Step 2 & 3, the peg was buying stability but costing autonomy. Step 4, the trilemma: with a fixed rate plus free capital flow, the country had already given up independent monetary policy — so cutting rates triggers capital outflows, downward pressure on the currency, and reserve depletion as the central bank defends the line, until the peg becomes unsustainable. Four steps, no guesswork, no invented numbers.

A first-party note from the CNEC desk

As the officially authorized China test center for the NEC, the recurring pattern we see in practice rounds is that students treat “fixed” and “floating” as a simple good-versus-bad pair, then lose marks because they cannot say what each one costs. The teams that score well do two things: they always pair every benefit with its trade-off (stability is bought with lost autonomy; autonomy is bought with volatility), and they reach for the trilemma to explain why — identifying the two corners a country chose and the third it sacrificed. A third habit pays off in written rounds: framing a current-account or shock scenario by asking “where does the adjustment land?” (the currency under a float, the domestic economy under a peg), which signals structural understanding rather than a memorised label.

A standing reminder on facts: this article teaches the regime economics the world-economy section tests, which is stable theory. Anything competition-specific — the exact rounds in which these questions appear, the weighting, and the format for a given cycle — is set by the organiser and changes year to year, so confirm it on the official channels. The CEE sets the underlying academic standard for the NEC; the CNEC desk runs the China round. The CNEC is the official China National Round, operated by Hanlin (SKT) since 2016 across 20+ provinces and 300+ schools, and it is the only official path from China to the NEC global rounds. You can review the official details on the official CNEC site; any named question-setters or judges cited elsewhere are organiser claims to confirm officially, never to assert as fact.

Frequently asked questions

What is an exchange-rate regime?

The rule a country follows for valuing its currency — fixed (a defended peg), floating (set by the market), or managed (mostly market-led with occasional intervention).

What is the main trade-off between fixed and floating?

A fixed rate buys stability but largely surrenders independent monetary policy; a float keeps policy freedom but accepts exchange-rate volatility.

What is the policy trilemma the NEC tests?

A country cannot have all three of a fixed rate, free capital movement and independent monetary policy at once — it must pick two and give up the third.

Why can a fixed peg with open capital markets be forced to break?

With those two corners chosen, the country has no policy autonomy, so an interest-rate cut sparks capital outflows and reserve loss until the peg fails.

Published by the NEC / CNEC editorial desk, operated by Hanlin Education as the officially authorized China National Economics Challenge (CNEC) test center. The NEC is run by the Council for Economic Education, which sets the official rules — always confirm current dates, divisions, fees and awards on the official CNEC channels. Any errors will be corrected within 7 working days.